Opera 50 now comes with built-in protection against cryptojacking

More and more websites are monetizing their users via in-browser cryptocurrency mining. Instead of showing intrusive adverts, the site instead takes advantage of the user’s CPU power to solve mathematical problems, which are then used to create valuable digital coins.

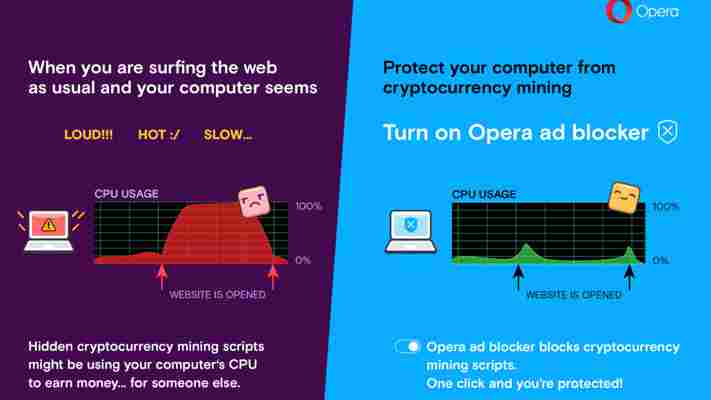

This is called “cryptojacking,” and it isn’t particularly great for users, who find their machines become inexplicably sluggish.

Mercifully, the latest version of the Opera browser comes with built-in protections against cryptojacking. Opera 50 uses the No Coin list, which is updated regularly as new mining scripts emerge.

To activate it, simply turn on the browser’s built-in adblocker in preferences. If you wish to view adverts (some websites take a dim view on adblocking) but want to protect yourself against cryptojacking, simply tick the “No Coin” box.

In a statement, Krystian Kolondra, head of Desktop Browser at Opera, said:

It couldn’t come at a better time. Cryptojacking is a worrying trend. A study from AdGuard published in November 2017 found that 33,000 sites used crypto-coin mining scripts as a monetization tactic. AdGuard estimates that these sites reach as many as one billion people each month.

And it’s only getting worse. AdGuard looked at the 100,000 most popular websites (according to analytics firm Alexa), and discovered that the number of sites using cryptojacking is growing 31 percent month-on-month.

Opera has the distinction of being first browser to address the issue by adding built-in cryptojacker protections, but I doubt it’ll be the last.

Starting from February 15th, Google Chrome will come with an integrated ad-blocker . This was largely a response to widespread consumer malcontent at the state of the online advertising industry. As the general public become more aware of cryptojacking, you can expect them (and other browser developers) to follow suit.

Opera 50 is available from today, and you can download it here .

Going beyond Bitcoin wallets: These apps give you better control over your cryptocurrency-based finances

Bitcoin is a great technology, right? It is decentralized, it’s cheap to transact, and no government or central bank has control over it. And one other thing, its value seems to be skyrocketing, which means it might be a good time to jump on the bandwagon and use it both as an investment and as a means to transact.

However, don’t convert your entire life savings to crypto just yet. While Bitcoin and other cryptocurrencies have already become mainstream, there are still some challenges ahead. And even with blockchain-powered technologies making life simpler and easier for users, it pays to have a better understanding of what makes cryptocurrencies and blockchains tick, and how we users can actually take advantage.

For one, there is no doubt that cryptocurrencies like Bitcoin and Ethereum are seeing mainstream use through apps and mobile solutions. But it is not always a rosy picture in terms of using this digital money.

In my earlier articles, I took a look at the potentials of blockchain for businesses , in making investments , and even addressing global poverty by giving financial access to the unbanked. But there is a simpler question for us users of cryptocurrencies.

Why can’t I just spend my coins?

The biggest benefit of Bitcoin, Ethereum, and other cryptocurrencies is also its biggest challenge: the fact that it is a purely digital currency. This means the amount in circulation is as digital as the cryptography that has created it — there are no paper bills or coins in circulation. While a unit of BTC or ETH may have its equivalent exchange in fiat currencies like the US dollar, there are no physical reserves of the currency.

The need to spend and exchange coins (for simplicity, we will refer to units of cryptocurrencies simply as coins) has spawned an entire industry of exchanges, where individuals, companies and platforms exchange coins with fiat money (like the US dollar, British pound, Euro, etc.).

Activity on exchanges like Coinbase also influence the value of coins. More transaction (velocity) influences the price upwards. In many cases, when exchanges are compromised by hacks and traffic attacks, cryptocurrency values also take a downward hit.

In the early days, this has mostly been peer-to-peer, with users exchanging their coins to dollars and vice versa through methods like bank transfers and sometimes even through in-game currency. Now, apps are letting us do all sorts of things, from paying bills to sending money to friends, and even shopping using funds from our Bitcoin wallet. Here’s how.

Bitcoin for debit card payments

The biggest benefit of Bitcoin should be how you can spend it, right? While some online stores and sellers already accept Bitcoin as a means of payment, how about the millions of stores and merchants out there that do not? You can’t just show the cashier the transaction confirmation from your Bitcoin wallet — most people do not even know what Bitcoin is.

One startup currently making its mark is CryptoPay , which is making it easy to spend all that cryptocurrency at just about any store with a credit card terminal. CryptoPay is essentially a Bitcoin wallet platform, but it does more than hold your coins for you. One of its main features is the CryptoPay debit card, which is a Visa card that you can use to pay for purchases.

The company has two versions — a physical card that you can swipe (or insert into EMV terminals) and a virtual card you can use for transactions. Either way, both of these are a convenient way to spend your coins on any store without thinking about manually converting these or looking for someone who can buy your Bitcoins.

Bitcoin for your salary

Still working the daily 9-5 grind? Or maybe you are working as a freelancer or remote professional. You might be happy to learn that there are platforms that cater to your crowd. A company called BitWage offers a solution that lets employers pay wages directly to the employees’ cryptocurrency wallets.

These services make it faster to settle wages, compared to legacy systems that require lengthy bank transfers. For freelancers with international clients, this solution offers a cheaper and faster means to receive salaries, compared with traditional bank transfers. The platform even provides tools for employers to manage their remote workforce.

“Workforces are increasingly becoming decentralized,” says Jonathan Chester , founder and CEO at BitWage. “Payments and trust are areas where Bitcoin and the blockchain offer an advantage.”

Accept Bitcoin from customers

Now the other side of the coin (see what I did there?) is accepting cryptocurrencies as a means of payment if you are running a business. Understandably, setting up yet another payment method might be taxing in terms of cost and onboarding involved. The above-mentioned CryptoPay actually offers this service, offering API access so that you can incorporate Bitcoin payments into your business website or platform.

Another option is e-commerce service Shopify , which offers a white-label solution wherein you can establish your own branded store with multiple payment options — yes, Bitcoin included!

Make or raise a coin-based investment

Sure, people are going crazy over how Bitcoin’s value has more than doubled just this May 2017 from $1,300 to around $2,700. However, seasoned investors, entrepreneurs and venture capitalists are now more interested in how businesses can use cryptocurrencies and the blockchain to raise capital for their businesses.

Herein lies the potential of initial coin offerings or ICOs, which enable businesses to crowdfund capital using cryptographic tokens and leveraging on the value gained from buying these at a discount. However, with the number of ICOs being launched, the question is whether this is a viable means of growing capital for investors.

According to George Basiladze, Founder and CEO at CryptoPay, it’s a matter of properly executing an ICO and ensuring its sustainability. “Many companies are launching their ICOs at early stages, but we believe that the companies that will benefit from an ICO are those that already have products that already work with business models that are already tested,” he says.

He adds that it is also a good idea to do due diligence not only on the company but also on the people investing in the ICO. “In our case, only verified users are allowed to invest in our upcoming ICO. We also plan to tie the ICO to the CryptoPay service performance metrics, which means that the tokens each person could get would be tied to their contribution and engagement in the platform.”

In conclusion

Bitcoin and other cryptocurrencies have the power to touch the lives of practically anyone. It’s a matter of finding practical applications and practical tools that give value to its users. The financial tools I mentioned here are truly empowering as they can potentially change lives by helping people save on fees, earn a decent living, and even make a small investment. It’s a matter of taking advantage of the technology even without an in-depth knowledge of how it works.

Blockchain is crappy technology and a bad vision for the future

This December I wrote a w i d e l y- c i r c u l a t e d article on the inapplicability of blockchain to any actual problem. People objected mostly not to the technology argument, but rather hoped that decentralization could produce integrity .

Let’s start with this: Venmo is a free service to transfer dollars, and bitcoin transfers are not free. Yet after I wrote an article last December saying bitcoin had no use, someone responded that Venmo and Paypal are raking in consumers’ money and people should switch to bitcoin.

What a surreal contrast between blockchain’s non-usefulness/non-adoption and the conviction of its believers! It’s so entirely evident that this person didn’t become a bitcoin enthusiast because they were looking for a convenient, free way to transfer money from one person to another and discovered bitcoin. In fact, I would assert that there is no single person in existence who had a problem they wanted to solve, discovered that an available blockchain solution was the best way to solve it, and therefore became a blockchain enthusiast.

The number of retailers accepting cryptocurrency as a form of payment is declining , and its biggest corporate boosters like IBM , NASDAQ , Fidelity , Swift , and Walmart have gone long on press but short on actual rollout. Even the most prominent blockchain company, Ripple, doesn’t use blockchain in its product . You read that right: the company Ripple decided the best way to move money across international borders was to not use Ripples .

A blockchain is a literal technology, not a metaphor

Why all the enthusiasm for something so useless in practice?

People have made a number of implausible claims about the future of blockchain—like that you should use it for AI in place of the type of behavior-tracking that google and facebook do, for example. This is based on a misunderstanding of what a blockchain is.

A blockchain isn’t an ethereal thing out there in the universe that you can “put” things into, it’s a specific data structure: a linear transaction log, typically replicated by computers whose owners (called miners) are rewarded for logging new transactions.

There are two things that are cool about this particular data structure. One is that a change in any block invalidates every block after it, which means that you can’t tamper with historical transactions. The second is that you only get rewarded if you’re working on the same chain as everyone else, so each participant has an incentive to go with the consensus.

The end result is a shared definitive historical record. And, what’s more, because consensus is formed by each person acting in their own interest, adding a false transaction or working from a different history just means you’re not getting paid and everyone else is. Following the rules is mathematically enforced—no government or police force need come in and tell you the transaction you’ve logged is false (or extort bribes or bully the participants). It’s a powerful idea.

So in summary, here’s what blockchain-the-technology is:

Now, here’s what blockchain-the-metaphor is: “What if everyone keeps their records in a tamper-proof repository not owned by anyone?”

An illustration of the difference: In 2006, Walmart launched a system to track its bananas and mangoes from field to store. In 2009 they abandoned it because of logistical problems getting everyone to enter the data, and in 2017 they re-launched it (to much fanfare ) on blockchain.

If someone comes to you with “the mango-pickers don’t like doing data entry,” “I know: let’s create a very long sequence of small files, each one containing a hash of the previous file” is a nonsense answer, but “What if everyone keeps their records in a tamper-proof repository not owned by anyone?” at least addresses the right question!

Blockchain-based trustworthiness falls apart in practice

People treat blockchain as a “futuristic integrity wand”—wave a blockchain at the problem, and suddenly your data will be valid. For almost anything people want to be valid , blockchain has been proposed as a solution.

It’s true that tampering with data stored on a blockchain is hard, but it’s false that blockchain is a good way to create data that has integrity.

To understand why this is the case, let’s work from the practical to the theoretical. For example, let’s consider a widely-proposed use case for blockchain: buying an e-book with a “smart” contract. The goal of the blockchain is, you don’t trust an e-book vendor and they don’t trust you (because you’re just two individuals on the internet), but, because it’s on blockchain, you’ll be able to trust the transaction.

In the traditional system, once you pay you’re hoping you’ll receive the book, but once the vendor has your money they don’t have any incentive to deliver. You’re relying on Visa or Amazon or the government to make things fair—what a recipe for being a chump!

In contrast, on a blockchain system, by executing the transaction as a record in a tamper-proof repository not owned by anyone, the transfer of money and digital product is automatic, atomic, and direct, with no middleman needed to arbitrate the transaction, dictate terms, and take a fat cut on the way. Isn’t that better for everybody?

Hm. Perhaps you are very skilled at writing software. When the novelist proposes the smart contract, you take an hour or two to make sure that the contract will withdraw only an amount of money equal to the agreed-upon price, and that the book — rather than some other file, or nothing at all — will actually arrive.

Auditing software is hard! The most-heavily scrutinized smart contract in history had a small bug that nobody noticed — that is, until someone did notice it, and used it to steal fifty million dollars. If cryptocurrency enthusiasts putting together a $150m investment fund can’t properly audit the software, how confident are you in your e-book audit?

Perhaps you would rather write your own counteroffer software contract, in case this e-book author has hidden a recursion bug in their version to drain your ethereum wallet of all your life savings?

It’s a complicated way to buy a book! It’s not trustless , you’re trusting in the software (and your ability to defend yourself in a software-driven world), instead of trusting other people.

Another example: the purported advantages for a voting system in a weakly-governed country. “Keep your voting records in a tamper-proof repository not owned by anyone” sounds right — yet is your Afghan villager going to download the blockchain from a broadcast node and decrypt the Merkle root from his Linux command line to independently verify that his vote has been counted? Or will he rely on the mobile app of a trusted third party — like the nonprofit or open-source consortium administering the election or providing the software?

These sound like stupid examples — novelists and villagers hiring e-bodyguard hackers to protect them from malicious customers and nonprofits whose clever smart-contracts might steal their money and votes?? — until you realize that’s actually the point .

Instead of relying on trust or regulation, in the blockchain world, individuals are on-purpose responsible for their own security precautions. And if the software they use is malicious or buggy, they should have read the software more carefully.

The entire worldview underlying blockchain is wrong

You actually see it over and over again. Blockchain systems are supposed to be more trustworthy, but in fact, they are the least trustworthy systems in the world . Today, in less than a decade, three successive top bitcoin exchanges have been hacked, another is accused of insider trading, the demonstration-project DAO smart contract got drained , crypto price swings are ten times those of the world’s most mismanaged currencies, and bitcoin, the “killer app” of crypto transparency, is almost certainly artificially propped up by fake transactions involving billions of literally imaginary dollars .

Blockchain systems do not magically make the data in them accurate or the people entering the data trustworthy, they merely enable you to audit whether it has been tampered with.

A person who sprayed pesticides on a mango can still enter onto a blockchain system that the mangoes were organic. A corrupt government can create a blockchain system to count the votes and just allocate an extra million addresses to their cronies. An investment fund whose charter is written in software can still misallocate funds.

How then, is trust created?

In the case of buying an e-book, even if you’re buying it with a smart contract, instead of auditing the software you’ll rely on one of four things, each of them characteristics of the “old way”: either the author of the smart contract is someone you know of and trust, the seller of the e-book has a reputation to uphold , you or friends of yours have bought e-books from this seller in the past successfully, or you’re just willing to hope that this person will deal fairly.

In each case, even if the transaction is effectuated via a smart contract, in practice you’re relying on trust of a counterparty or middleman, not your self-protective right to audit the software, each man an island unto himself. The contract still works, but the fact that the promise is written in auditable software rather than government-enforced English makes it less transparent, not more transparent.

The same for the vote counting. Before blockchain can even get involved, you need to trust that voter registration is done fairly, that ballots are given only to eligible voters, that the votes are made anonymously rather than bought or intimidated, that the vote displayed by the balloting system is the same as the vote recorded, and that no extra votes are given to the political cronies to cast.

Blockchain makes none of these problems easier and many of them harder—but more importantly, solving them in a blockchain context requires a set of awkward workarounds that undermine the core premise. So we know the entries are valid, let’s allow only trusted nonprofits to make entries—and you’re back at the good old “classic” ledger. In fact, if you look at any blockchain solution, inevitably you’ll find an awkward workaround to re-create trusted parties in a trustless world.

A crypto-medieval system

Yet absent these “old way” factors—supposing you actually attempted to rely on blockchain’s self-interest/self-protection to build a real system—you’d be in a real mess.

Eight hundred years ago in Europe — with weak governments unable to enforce laws and trusted counterparties few, fragile and far between — theft was rampant, safe banking was a fantasy, and personal security was at the point of the sword. This is what Somalia looks like now, and also, what it looks like to transact on the blockchain in the ideal scenario .

Somalia on purpose. That’s the vision. Nobody wants it!

Even the most die-hard crypto enthusiasts prefer in practice to rely on trust rather than their own crypto-medieval systems. 93% of bitcoins are mined by managed consortiums, yet none of the consortiums use smart contracts to manage payouts. Instead, they promise things like a “long history of stable and accurate payouts.” Sounds like a trustworthy middleman!

Same with Silk Road, a cryptocurrency-driven online drug bazaar. The key to Silk Road wasn’t the bitcoins (that was just to evade government detection), it was the reputation scores that allowed people to trust criminals. And the reputation scores weren’t tracked on a tamper-proof blockchain, they were tracked by a trusted middleman!

If Ripple, Silk Road, Slush Pool, and the DAO all prefer “old way” systems of creating and enforcing trust, it’s no wonder that the outside world had not adopted trustless systems either!

In the name of all blockchain stands for, it’s time to abandon blockchain

A decentralized, tamper-proof repository sounds like a great way to audit where your mango comes from, how fresh it is, and whether it has been sprayed with pesticides or not.

But actually, laws on food labeling, nonprofit or government inspectors, an independent, trusted free press, empowered workers who trust whistleblower protections, credible grocery stores, your local nonprofit farmer’s market, and so on, do a way better job.

People who actually care about food safety do not adopt blockchain because trusted is better than trustless. Blockchain’s technology mess exposes its metaphor mess — a software engineer pointing out that storing the data a sequence of small hashed files won’t get the mango-pickers to accurately report whether they sprayed pesticides is also pointing out why peer-to-peer interaction with no regulations, norms, middlemen, or trusted parties is actually a bad way to empower people.

Like the farmer’s market or the organic labeling standard, so many real ideas are hiding in plain sight.

Do you wish there was a type of financial institution that was secure and well-regulated in all the traditional ways, but also has the integrity of being people-powered? A credit union’s members elect its directors, and the transaction-processing revenue is divided up among the members. Move your money!

Prefer a deflationary monetary policy? Central bankers are appointed by elected leaders. Want to make elections more secure and democratic? Help write open source voting software, go out and register voters, or volunteer as an election observer here or abroad!

Wish there was a trusted e-book delivery service that charged lower transaction fees and distributed more of the earnings to the authors? You can already consider stated payout rates when you buy music or books, buy directly from the authors, or start your own e-book site that’s even better than what’s out there!

Projects based on the elimination of trust have failed to capture customers’ interest because trust is actually so damn valuable . A lawless and mistrustful world where self-interest is the only principle and paranoia is the only source of safety is a not a paradise but a crypto-medieval hellhole.

As a society, and as technologists and entrepreneurs, in particular, we’re going to have to get good at cooperating — at building trust, and, at being trustworthy. Instead of directing resources to the elimination of trust, we should direct our resources to the creation of trust—whether we use a long series of sequentially hashed files as our storage medium or not.

Leave a Comment